Increased Listings Offer More Choices for Buyers this April

In this report, we'll be breaking down the April stats provided by the Toronto Regional Real Estate Board (TRREB). They are specifically for the City of Toronto which includes Etobicoke, Central Toronto, North York, East York and Scarborough.

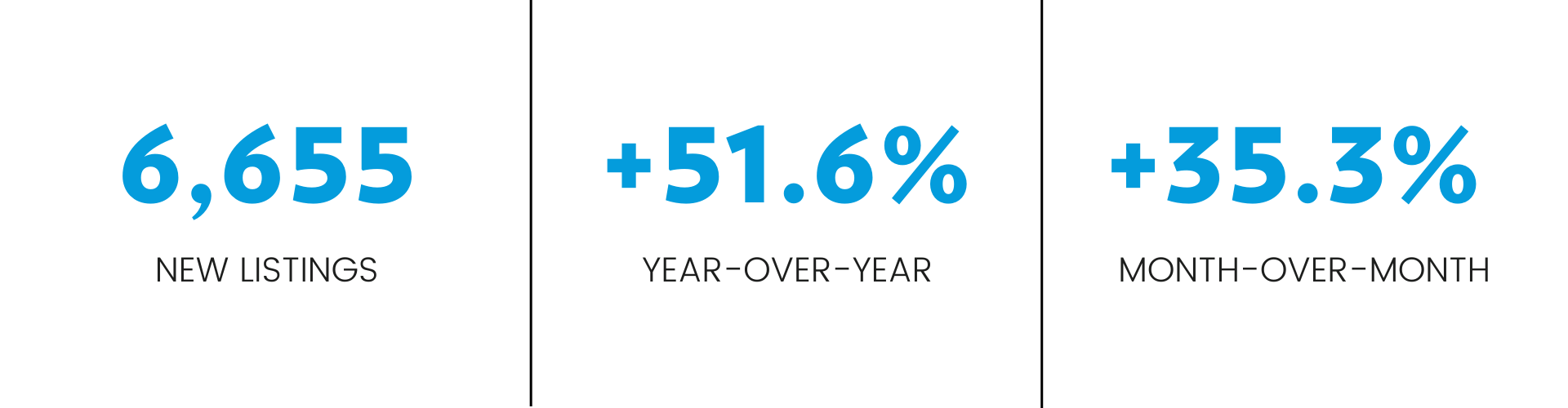

In April, the momentum from March's increase in new listings carried forward, with strong year-over-year and month-over-month growth. This rising trend showcases growing seller confidence as the weather heats up.

“Listings were up markedly in April in comparison to last year and last month. Many homeowners are anticipating an increase in demand for ownership housing as we move through the spring. While sales are expected to pick up, many would-be home buyers are likely waiting for the Bank of Canada to actually begin cutting its policy rate before purchasing a home,” said TRREB President Jennifer Pearce.

We're noticing a blend of "offers anytime" and "offer date" scenarios unfolding across various communities and market segments throughout the City of Toronto. Movement remains particularly noticeable in the most coveted neighbourhoods and micro-markets across the city, reflecting the dynamic nature of the current market.

In April 2024, home sales activity dipped slightly compared to the same period last year. However, month-over-month sales have been trending upward, signalling growing momentum. It will be interesting to see what happens in the summer, traditionally a slower period for real estate, if interest rates finally start to drop. Such a shift could further fuel the upward trend in sales, potentially extending the current momentum beyond spring.

Since the start of the year, the average sale price in Toronto has been on a gradual incline. This April, the city recorded an average sale price of $1,152,200, marking a continued trend of growth both year-over-year and month-over-month.

If new listings continue to outpace sales, the increased inventory could lead to more competitive pricing among sellers, potentially causing a slowdown in price growth or even a dip in prices. Much will also hinge on other key factors, including interest rates, which the Bank of Canada will address in its next announcement on June 5th. Buyers and sellers should be watching closely to see how these factors affect demand, negotiation power, and pricing dynamics across the different segments of the market.

Understanding key real estate market metrics: sales-to-new-listing ratio, days on market, and months of inventory:

The sales-to-new-listing ratio (SNLR) tells us how many of the newly listed properties are being sold in a certain time frame. If the ratio is around 50%, it means the market is balanced. But if it goes above 60%, that's when we start to see a seller's market, where prices tend to rise. So, the higher the ratio, the better it is for sellers and the more competitive the market becomes for buyers.

The average days on market (DOM) refers to the average amount of time that it takes for a property to be sold after it is listed for sale. This can be a useful metric for understanding how quickly homes are being snapped up in a particular area.

Lastly, the months of inventory (MOI) is a measure of the amount of time it would take for all of the currently listed properties to be sold, based on the current rate of sales. It's a useful metric for understanding how much supply there is relative to demand in a particular area. For example, if there are 100 properties currently listed for sale and 20 of them are sold each month, it would take 5 months to sell all of the properties (100 / 20 = 5).

With new listings significantly outpacing sales this month, the Sales-to-New Listings Ratio (SNLR) has fallen once more, pushing us deeper into a buyer's market. This shift indicates that buyers now have more leverage and a greater selection of properties to choose from, potentially leading to more competitive pricing and favourable negotiation conditions.

Ultimately, the degree of leverage and competitive pricing will vary depending on the specific type of property and its location.

In April 2024, the Average Days on Market (DOM) fell by one day compared to the previous month but rose by three days year-over-year. The DOM has been decreasing since the start of the year, reflecting an uptick in market activity as buyers make offers and close deals a little more quickly. However, homes are still staying on the market longer than they were last year.

Despite this, the steady decline in monthly DOM indicates a market gaining momentum and gearing up for potential increases in activity, particularly if interest rates fall and further encourage buyer engagement.

Not surprisingly, the Months of Inventory (MOI) has increased both year-over-year and month-over-month. This rising MOI indicates that despite growing activity, reflected in the slight drop in the Average Days on Market (DOM), the surge in new listings combined with slower sales is keeping inventory levels high.

As we monitor these trends, all eyes are on the Bank of Canada's interest rate announcement on June 5th. A decrease in interest rates could potentially accelerate sales, allowing the market to absorb the rising inventory, thus reducing the MOI. Such a shift would likely balance or even improve the Sales-to-New Listings Ratio (SNLR), potentially signalling a shift toward a seller’s market if sales outpace the growth in new listings.

Overall, the current market remains dynamic and complex, with a mix of competitive opportunities and favourable negotiation conditions across various segments. Buyers and sellers are both adjusting their strategies to navigate the evolving conditions, which will continue to be shaped by seasonality, economic developments, interest rate changes, and shifting buyer preferences in the months ahead.

If you have any questions or would like more information on recent home sales in your specific neighbourhood, don't hesitate to connect with us here.